Real estate vs. Bitcoin: Dismantling The Cash-Flow Narrative

The Bitcoin Newsletter 18

Welcome to the 18th edition of The Bitcoin Newsletter,

Bitcoin skeptics frequently argue that bitcoin lacks intrinsic value, claiming that investments like real estate, with their tangible cash flows, are superior. In this extended edition of the newsletter’s Deep Dive section, I aim to debunk the myth of 'intrinsic value' and illustrate why cash flow does not directly impact an asset's capacity to serve as a reliable store of value, even in the context of real estate.

Furthermore, as highlighted in the Worth to Know section, I'm pleased to have been featured on several podcasts and authored some articles, including “Bitcoin vs. Real Estate – Which is the Better Store of Value in Times of Conflict?”.

As always, feel free to share any feedback with me as I highly appreciate it. Thank you for joining me in exploring the intricacies of Bitcoin and its role in the broader financial landscape.

Best regards,

Leon

DEEP DIVE

Dismantling the cash flow narrative

The journey of writing my book on Bitcoin and real estate led me to explore the widely-held believe that things have intrinsic value and that real estate, with its tangible cash flow, reigns supreme over bitcoin as an investment. I have already challenged this narrative through insights I discussed with Austrian Bitcoin podcaster Niko Jilch a few months ago, who recently published an excellent explanation in German debunking the myth of intrinsic value.

WATCH | WATCH

The myth of intrinsic value

The idea that value is inherently embedded in objects - with the value of an item tied to the labor, output or energy invested - is a misconception.

This belief, rooted in the Labor Theory of Value (LTV), suggests that labor determines value, a flawed concept used in both Marxism and modern economic theories.

This belief extends to real estate, with the notion that its ability to generate cash flow through rentals or its utility as a living and production space imbues it with intrinsic value. But, the concept of intrinsic value is fundamentally flawed.

Subjectivity of value

In a free market, characterized by voluntary exchanges, it's evident that value is subjective. Both parties involved in a transaction believe that what they receive is of greater value than what they give up, indicating that value is determined by individual perception rather than inherent qualities.

Take the Rolex watch as an example: its value is not merely a reflection of the extensive labor involved in its craftsmanship but is significantly influenced by its scarcity and the aspiration among individuals to own it. This principle of subjective valuation extends across the board; the worth of assets, including bitcoin and real estate, is not predetermined but fluctuates based on personal perceptions of value.

Understanding the subjectivity of value is crucial for grasping the true essence of bitcoin's value, illustrating that its significance, much like that of real estate or luxury watches, is deeply rooted in the collective demand and limited availability, rather than inherent properties.

Among others, Carl Menger, a pioneer of the Austrian School of Economics and arguably an inspiration behind the Cypherpunks' creation of Bitcoin, demonstrated already in the 19th century that prices are a reflection of subjective valuation.

The Subjective theory of value parallels the perception of beauty, which is also in the eye of the beholder. Just as beauty standards vary, so does the value of objects like bitcoin, which are coveted not for their inherent value but for people's collective desire or need to possess them.

The absence of intrinsic value is a fundamental economic principle, crucial for understanding why Bitcoin holds value. And vice versa. A lack of understanding of this prevents understanding Bitcoin.

Bitcoin's value proposition

The value of bitcoin does not come from the difficulty of its production, but rather comes from the unparalleled protection the network gives to the value stored within it and the network's final settlement capabilities, which creates demand for bitcoin as an asset. Bitcoin is, besides time, the first absolute scarce commodity that we discovered in this universe. This scarcity, highlighted by a disinflationary issuance schedule and the virtually indestructible network, is driving demand for bitcoin.

Real Estate’s value proposition

In numerous real estate transactions, I experienced that investors typically assume the majority of profits originate from property appreciation rather than direct cash flow.

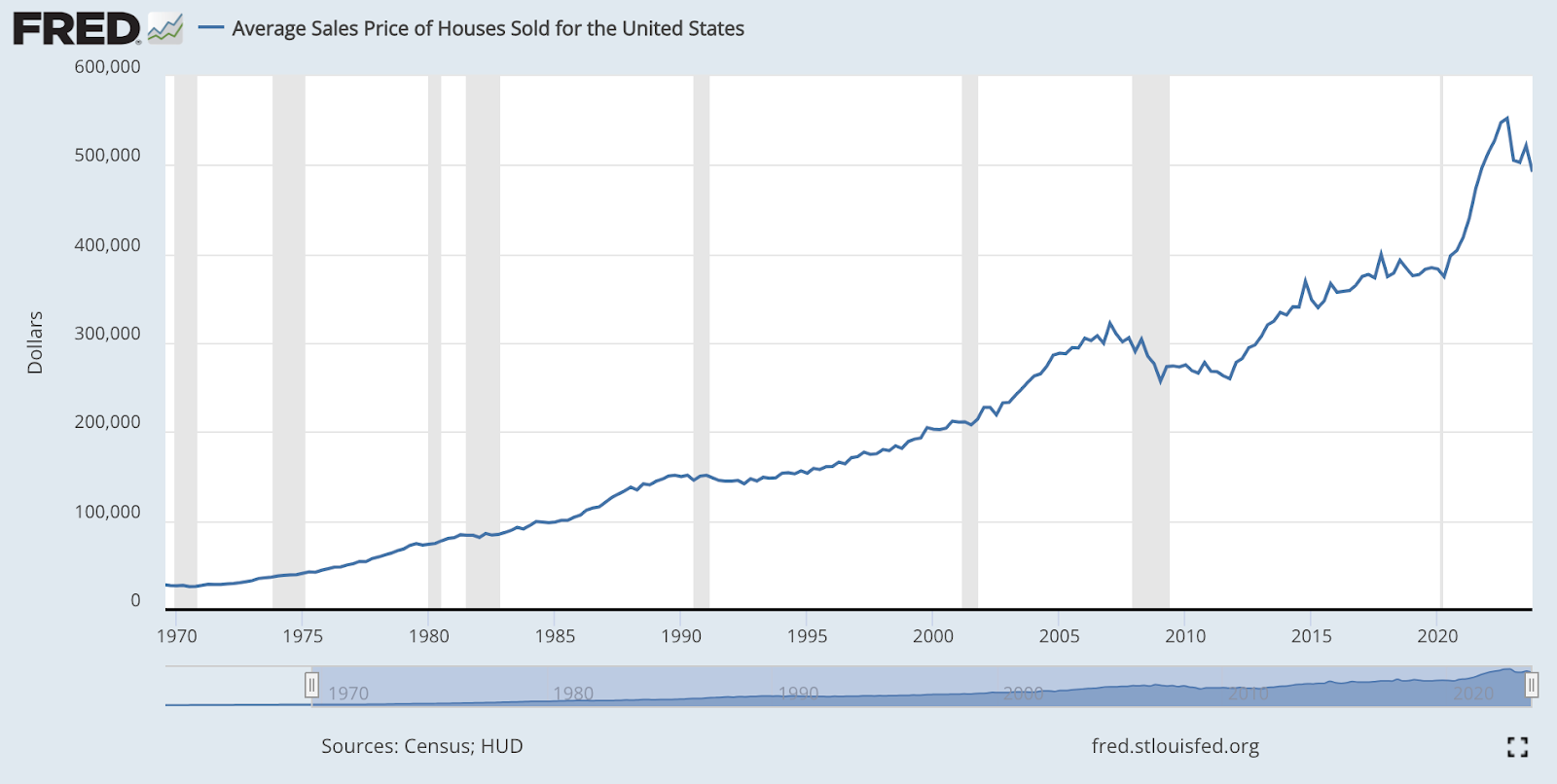

This observation underscores a critical insight: real estate's high valuation is less about the immediate income it can generate and more about its scarcity and ability to hedge against inflation. This observation can be confirmed when one looks at the data on the increase in the price of houses and the money supply (M2) in the U.S.

The following chart, depicting the average sales price of houses sold in the U.S., illustrates a sharp increase in housing prices since 1971. The average sales price of a house in the U.S. rose from ≈$27,000 in 1971 to ≈$492,000 in the third quarter of 2023, indicating a substantial appreciation in property values over this period (≈1,700%).

This period follows the Federal Reserve's transition to a fiat currency system initiated on August 15, 1971, when U.S. President Richard Nixon announced the United States would end the convertibility of the dollar into gold. Subsequently, central banks globally adopted a fiat-based monetary system characterized by floating exchange rates and the absence of currency standards.

As illustrated in the following chart, the money supply (M2) has exhibited a consistent increase since the detachment of the U.S. dollar from gold. This vividly illustrates the striking correlation between the escalation of housing prices and the concurrent expansion of the U.S. money supply. M2, as defined by the Federal Reserve, encompasses a broad spectrum of the money supply, including cash, checking deposits, and easily convertible liquid assets like certificates of deposit (CDs).

Analyzing the compound annual growth rates (CAGR) of these two metrics shows a clear connection between them. Since 1971, the money supply (M2) has experienced a compound annual growth rate (CAGR) of 6.9%, closely paralleled by housing prices, which have risen at a CAGR of 5.7% (for the detailed calculation breakdown, please see the resource section). Why did this happen ? The increase in the money supply forced market participants to look for ways to invest their money to protect against this monetary inflation and one of the most popular investments has been real estate.

The correlation between the expansion of the money supply (M2) and rising housing prices is influenced by several factors, including interest rates, economic growth, and housing supply dynamics. Since 1971, however, phases of rapid monetary expansion have usually been accompanied by low interest rates and increased borrowing.

The availability of affordable financing increases buyers' purchasing power and, consequently, demand, particularly because housing is predominantly acquired through loans. This surge in demand, in turn, drives up real estate prices.

This phenomenon is evident globally. Influenced by the historical role of the United States as the leading world power, setting a precedent with the dollar as the world reserve currency. Although, there are exceptions like Japan, where an aging population has led to an oversupply of housing and falling prices. Only in some metropolitan regions such as Tokyo is real estate still used to store value.

Despite these regional differences, a global trend emerges, real estate is used as a store of value in response to diminishing purchasing power caused by monetary supply expansion. It follows that the primary appeal of real estate, especially in high-demand locations, lies in its perceived ability to maintain value over time, a characteristic now challenged by Bitcoin's emergence.

Real Estate vs. Bitcoin

As the data shows, the excessive demand for real estate is due to monetary inflation, which has led people to invest in scarce assets such as real estate to protect their wealth. The primary role of a property's cash flow is in the repayment of loans, a topic I will explore in greater detail later.

The development of real estate prices reflects the financialization of the asset class, a development that was significantly influenced by the departure of central banks from the gold standard, marked by the “Nixon shock” in 1971.

This pivotal moment ushered in an era of unseen monetary expansionism. Real estate served as a relatively scarce store of value to protect wealth from the resulting inflation.

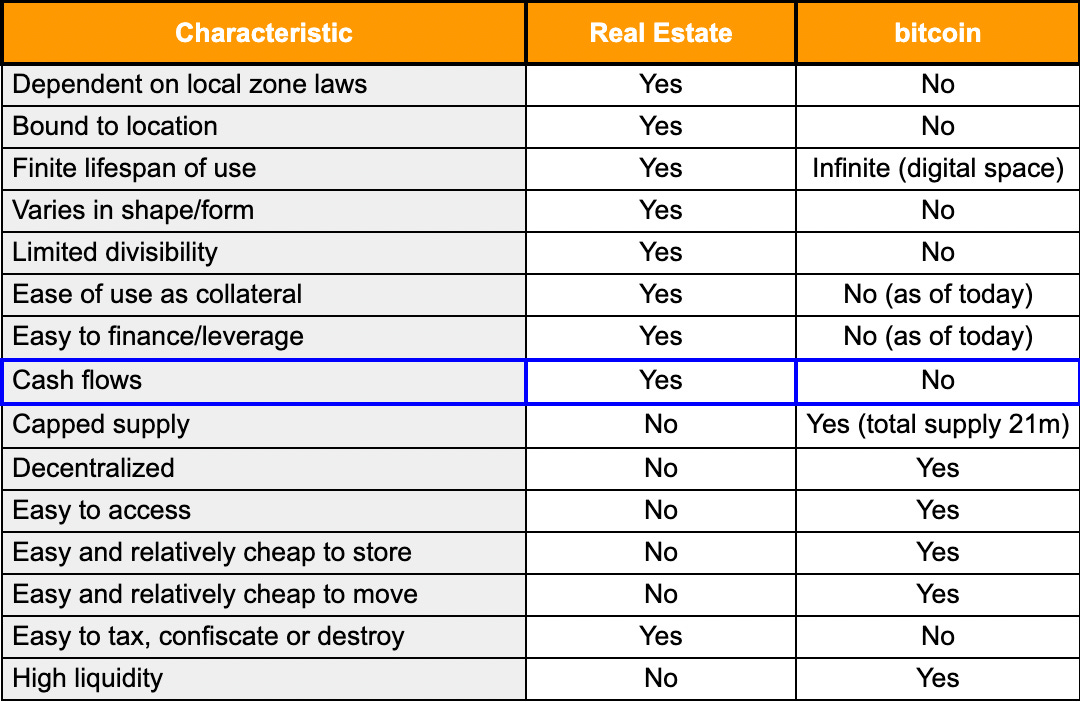

In its function as a store of value, real estate is in direct competition with bitcoin. A near perfect digital store of value. In consequence, real estate cannot compete with bitcoin as a store of value. The latter is rarer (capped in supply), cheaper to maintain, more liquid, easier to move and harder to confiscate, tax or destroy.

The comparative analysis of real estate and bitcoin in their function as a store of values underscores bitcoin's distinctive advantages.

Below, a succinct table highlights these differences, illustrating why bitcoin is emerging as a formidable competitor in the realm of value preservation.

The table highlights bitcoin as an exceptional emerging store of value. It is revealed that real estate's popularity as an investment choice has largely been driven by affordable financing options and its ability to generate cash flow, facilitating the repayment of debts. Given that real estate acquisitions are mostly financed through credit, this has been a primary factor behind its widespread purchase.

From this perspective, cash flow neither gives real estate any intrinsic value (which does not exist) nor does it act as a phenomenal store of value. The asset acts much more as a kind of reservoir for new money that comes onto the market in the inflationary fiat system.

Bitcoin analyst Rapha Zagury (aka Alpha Zeta) has found that the Composite 20 Case-Shiller Home Price Index, which tracks home prices in 20 metropolitan areas across the U.S., rose just 2.3% in value when prices are adjusted for inflation. This does not include the deduction of taxes, transaction costs and maintenance fees. He found that only in specific metropolitan areas like South Florida and Los Angeles, real estate prices have risen significantly faster than inflation, at a rate exceeding ≈4%.

In fact, bitcoin's qualities reflect many of real estate’s value offers on top of fundamentally more secure and easier custody, cheaper maintenance, absolute scarcity, resilience against inflation and most importantly the ability to protect, liquidate or move your wealth in times of crisis.

Real estate, while tangible and potentially yielding regular cash flow, is subject to regulatory changes, and physical degradation, factors that bitcoin inherently resists. If real estate is not properly cared for, its value will literally degrade over time. Bitcoin on the other hand provides the ultimate form of transferable value because it preserves the encapsulated wealth. If stored properly, its value will increase over time without high maintenance costs, as Michael Saylor likes to point out. WATCH

It cannot be denied that real estate as an asset class has certain advantages in the existing fiat system, since it has become increasingly important in the global financial system. After all, it is the world's number one store of value (≈67% of global wealth is stored in real estate) and collateral accepted by banks when granting loans. Therefore, many jurisdictions offer more robust financial infrastructures and tax advantages for purchasing real estate and utilizing it as collateral.

However, it is obvious that real estate cannot compete with bitcoin in its capacity as a store of value. Therefore, I expect that bitcoin's role as an indestructible, absolutely scarce store of value in the global financial system will become increasingly important and, due to its superiority over real estate, may lead to bitcoin replacing real estate in its role as the number one store of value in the distant future.

This is also expected to have a positive impact on its use as collateral. Both functions (store of value and collateral for lending) are closely linked. Why would a bank (or anyone else) accept collateral that loses value over the long term?

The infrastructure around access to financial services related to bitcoin and its use as collateral is still in its infancy. But the possibilities are extremely promising.

As a real estate developer, I see real estate as a business. We develop real estate and provide housing for which we receive rent in return. The cash flow is thus our return on investment (originary interest). However, the value of any object, including real estate, comes from its utility to the individual user. This is not to discount the benefits of cash flow, such as its role in repaying loans or covering living expenses. Yet, these aspects do not directly impact an asset's capacity to serve as a reliable store of value.

In my opinion, bitcoin enhances the real estate industry by offering a reliable store of value, safeguarding cash flows against monetary inflation. This advantage extends beyond real estate to encompass all sectors. As Michael Saylor, executive chairman and co-founder of software intelligence firm MicroStrategy, eloquently puts it, bitcoin represents the digital transformation of capital, marking a pivotal shift in how value is preserved across all industries.

During MicroStrategy's Q4 2023 earnings call, Michael Saylor highlighted the growing difficulty of generating cash flow that exceeds the rate of monetary inflation. He argued that in the context of the fiat system's widespread monetary inflation, relying on cash flow as an investment metric appears increasingly untenable. Saylor further underscored bitcoin's distinct role as a digital scarce asset, combining the value preservation qualities of real estate without its inherent drawbacks, thereby establishing it as an unparalleled store of value for the digital era.

According to Michael Saylor, one of bitcoin's greatest strengths lies in its valuation not being tethered to cash flow, rendering it immune to the adverse effects of inflation and quarterly financial reporting. On the contrary, bitcoin thrives in an environment of escalating fiat inflation, as it becomes a more attractive repository for capital. Its valuation mirrors the influx of capital flows, benefitting from the increased desire to safeguard wealth against the diminishing purchasing power of traditional fiat currencies.

Conclusion

In conclusion, the narrative of cash flow and intrinsic value in investment strategies is being reevaluated in the face of Bitcoin's rise. This digital asset, free from the constraints of traditional monetary systems, offers a glimpse into the future of finance, where value is preserved not in bricks but in bits.

As we navigate this transition, the lessons learned from the comparison between real estate and bitcoin will undoubtedly shape our approach to investment, wealth preservation, and the very fabric of the global financial system.

Ultimately, it's about an asset's DNA: its properties dictate how the value of the asset will trend over time (Myers, 2021).

Bitcoin, through its limited supply and decentralized nature, offers investors a digital fortress against the erosive forces of monetary inflation.

While real estate brings the opportunity to borrow money for the foreseeable future, it’s importance as a store of value should decline over time, while bitcoin, with its fixed supply and decentralized nature, is poised to become an increasingly preferred method for preserving wealth, offering unparalleled security and global accessibility without the constraints of traditional financial systems.

WORTH TO KNOW

Podcast and publications

Bitcoin Magazine: Bitcoin vs. real estate

In my latest article for Bitcoin Magazine, “Bitcoin vs. Real Estate – Which is the Better Store of Value in Times of Conflict?”, I analyze the different value propositions of bitcoin and real estate in times of geopolitical instability. I have also discussed this topic in this newsletter. READ

Have you ever wondered what lending would look like under a Bitcoin standard?

As part of my series of threads in which illustrate how Bitcoin could change the financial markets including real estate, interest rates and credit markets, I have published a thread in which I predict how Bitcoin could influence lending long-term. READ

Aprycot Media: Bitcoin as collateral

The German Bitcoin publisher Aprycot Media, known for its excellent translations of Bitcoin classics from English into German, published the German translation of my article “Why bitcoin is pristine collateral for lending,” originally published in Bitcoin Magazine on Sep. 13th, 2022. READ

Sell all real estate and buy bitcoin!?

Marc from the Hoten Princess in Plochingen, the first Bitcoin hotel in the world, recorded a very informative video in German on the topic of Bitcoin vs. real estate, in which I am featured. He also touches on some of the things I discussed with him and Niko Jilch on their respective podcasts. Here you can watch the respective videos in chronological order. WATCH | WATCH| WATCH

European Bitcoiners: Bitcoin ist kosher

The German translation of my article Bitcoin is kosher, (published in Bitcoin Magazine) which looks at Bitcoin from the perspective of Jewish faith and ethics, is now available on europeanbitcoiners.com, a platform for free Bitcoin education in almost all widely spoken European languages. READ

IDEAS OF INTEREST

Repricing the World in Bitcoin with Preston Pysh & Nico Lechuga - In this episode of "What Bitcoin Did" by Peter McCormack, Preston Pysh & Nico Lechuga, both partners at Bitcoin VC 'Ego Death Capital', explain how bitcoin, as a new unit of account, is revaluing markets, especially equities and company valuations. WATCH

Software intelligence company Microstrategy has presented its Q4 2023 earnings - CEO Phong Le announced that Microstrategy is the first Bitcoin development company in the world. WATCH

Broken Money Why Our Financial System Is Failing US And How We Can Make It Better Lyn Alden’s talk at Princeton about Broken Money is now on YouTube. As always, Lyn is worth listening to. WATCH

If you want to support me. Feel free. You can send me some satoshi/bitcoin.

My lightning address is: law@getalby.com

My bitcoin address is: bc1qyc9q89wjzmvaw729tj3wsrsfhft53mjycrjxdk

Nostr PubKey

npub1v5k43t905yz6lpr4crlgq2d99e7ahsehk27eex9mz7s3rhzvmesqum8rd9

Resources

Subjective-Value Theory

How Bitcoin Uses Energy by Leon A. Wankum

Nixon and the End of the Bretton Woods System, 1971–1973

From Bricks to Bits: Unmasking Real Estate Investment in the Bitcoin Era

Bitcoin As Property: What Perfection Looks Like with Michael Saylor | The Bitcoin Layer

McKinsey (2021) The rise and rise of the global balance sheet (how does the world store value?)

What Types Of Assets Might You Use For A Collateral-Based Loan?

Asset DNA: Explaining Bitcoin’s speculative attack on the dollar

To calculate the Compound Annual Growth Rate (CAGR) for both the Money Supply (M2) and housing prices, we used the formula:

CAGR = (Ending Value/Beginning Value)^(1/Number of Years)

For Money Supply (M2) from January 1971 to December 2023:

Beginning Value (Jan. 1971): $632.9 billion

Ending Value (Dec. 2023): $20,865 billion

Number of Years: 52

Substituting these values into the CAGR formula gives: CAGR= 6.9532%. Reflecting the annualized average growth rate of the total dollar money supply over this period.

Source: Growth Money Supply (M2) St. Louis FED

For housing prices from January 1971 to December 2023:

Beginning Value (Jan. 1971): $ 27,300

Ending Value (Dec. 2023): $ 492,300Number of Years: 52

Substituting these values into the CAGR formula gives: CAGR= 5.7195%. Reflecting the annualized average growth rate of housing prices in the U.S. over this period.

Source: Growth Average Sales Price of Houses Sold for the United States St. Louis FED

Photo Credit: Photographer: Joe Munroe/Archive Photos via Getty Images

Disclaimer: the content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Make sure you do your own research before making any investment and be aware of your own risk tolerance. If you like to build on my thoughts, feel free, but please cite me as the source. 2024 - Leon A. Wankum.

Editing and content creation by Clemens Haidinger.

0A79 E94F A590 C7C3 3769 3689 ACC0 14EF 663C C80B